![[Retire Early]](yourad.gif)

![[Retire Early]](retire.gif)

.

| ............. |

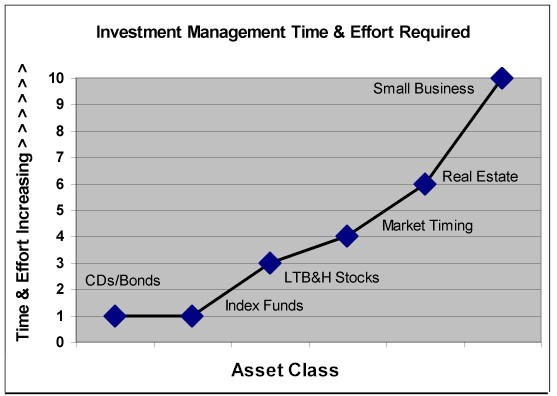

This article was first posted on December 1, 2001. Perhaps the most contentious issue surrounding early retirement is how to save and invest for early retirement. Some people made their money in real estate, others in the stock market, and a few even started successful businesses to fund their retirement. There are advantages and disadvantages to each type of investment. Your choice should depended on how much time you want to spend managing your investments and whether or not you possess the skills and psychological makeup necessary to be successful in that environment.

CDs or US Government Bonds Fixed income investments like bonds and CDs have historically under performed stocks for longer holding periods. Risk-adverse savers like them because of their low volatility and safety (in the case of US Government bonds or FDIC-insured CDs.) Unfortunately, they are unlikely to be a good bet for folks saving for retirement. Unless you are successful in identifying the few periods when bonds out perform stocks ahead of time, placing the majority of your retirement savings in fixed income investments will likely delay your retirement date. Fixed income investments are appropriate for one's "emergency fund", or if you are saving for an expediture that will take place in less than 5 years (say the purchase of an automobile or the down payment on a home.) And of course, once you're retired, you should keep a minimum of 5 years' worth of living expenses in cash and CDs. Index Funds Perhaps the easiest way to invest in the stock market is through an index fund. The Vanguard S&P500 index fund is the largest mutual fund available to investors in the United States. Low annual expenses and the opportunity to immediately diversify your investments among 500 of the largest companies in America are the principal attraction of this type of investment. In addition to the popular S&P500 index fund, there are small-cap index funds, international index funds, REIT index funds, and index funds that track several other asset classes. There's an ongoing debate on how diversified index fund investors need to be. Some experts like William J. Bernstein (author of The Intelligent Asset Allocator) advise wide diversification across as many as 9 asset classes. Other recognizable names like Vanguard's John C. Bogle and Berkshire Hathaway's Warren Buffett see little need to venture beyond an S&P500 index fund or the Wilshire 5000 (which one can track with the Vanguard Total Stock Market Index Fund.) Long-Term Buy & Hold (LTB&H) Individual Stocks Buying individual stocks is more time consuming and entails greater risk than holding an index fund, but gives investors a chance for higher returns. Unfortunately, no more than 1 out of 5 investors who hold individual stocks out perform the S&P500 index over the long term. As a matter of fact, most investors holding individual stocks would be better off with an index fund. One advantage of holding a LTB&H portfolio of individual stocks is the opportunity to reduce the fees and commissions you pay to almost zero. The lowest cost S&P500 index fund available to individual investors charges an annual fee of 0.10% of assets annually ($1,000 per $1 million invested.) LTB&H investors making only one or two trades per year could easily reduce their annual investment expenses to less than $100 per $1 million invested. Of course, that's only an advantage if you're among the 20% of investors that beat the S&P500 index. Market Timing The holy grail of finance is finding a system that places you in stocks when the market is rising and cash when stocks are declining. This investment technique is called market timing. An individual uncovering this Rosetta stone of investing would quickly amass great wealth. The financial world eagerly awaits the emergence of the first successful market timer and his enrollment in the Forbes 400 list of richest Americans. To date, that Pantheon contains mostly company founders and LTB&H types. While every once and a while a prominent market timer makes a good call, there is no evidence that market timers are successful over longer holding periods. Rental Real Estate Many people see the late-night infomercials on how to become a "No Money Down Real Estate Millionaire" and wonder if this might not be a path to early retirement. Certainly there are investors who've done well in real estate. Unfortunately, we have no way to determine the investment return for the "average guy who owns a rent house." Market statistics and reporting requirements for real estate investments do not approach the breadth and detail of those available for publicly-traded stocks and mutual funds.People who are successful in real estate stress the need to buy "well-selected properties". Good advice to be sure, but who holds all that property that was less than "well-selected" or located in neighborhoods seeing economic decline? No more than 20% of the investors who buy individual stocks out perform the S&P500 market average. Do more than 20% of real estate investors exceed this benchmark? No one knows. Transaction costs in real estate are far higher than other types of investments. While you can buy a $100,000 US Treasury security commission-free from Treasury Direct and $100,000 in stock from a discount broker for a commission of $10 to $15, a $100,000 home comes with a commission of 6% or $6,000. You have to see significant appreciation just to break even. Real estate investment requires active participation. Many successful real estate investors seem to handle one or more of the management and maintenance functions themselves. We're all familiar with "sweat equity" where real estate investors spend their nights and weekends performing the labor required to maintain and update their properties. Owners who lack mechanical skills may improve returns by handling the leasing of the property themselves instead of hiring a rental agent, or by doing their own accounting and legal work. The more duties you contract out instead of doing it yourself, the lower your investment return. Rental real estate does allow you to diversify beyond stocks and bonds but may not provide higher returns. It requires much more work than opening a brokerage statement at the end of the month. Make sure you understand what you're getting into before you add this asset class to your retirement portfolio. Many people who see the wisdom of adding real estate to their portfolios limit the time and hassle involved by purchasing a REIT index fund rather than individual properties.Small Business The entrepreneurial gene is relatively rare in the human population. If you are among the minority that possess the skills, patience, and drive necessary to operate your own business, your investment returns may well ellipse those available in other asset classes. However, there's a reason most small businesses fail and that most small business owners would make more money as someone else's employee. Only a few of us are suited for this type of activity. Lottery or Inheritance This category also includes winning a big insurance claim or personal injury case. It doesn't require much time or effort, but produces highly variable results. For example, in the case of an inheritance, how can you be sure your benefactor will die on schedule in time to fund your retirement? >  What did you do? I concentrated on limiting what I lose to fees and commissions and minimized the amount of time required to manage my investments. After dumping my mutual funds in 1989, my primary retirement investing vehicle was a diversified LTB&H portfolio of 10 to 15 stocks, mostly in the computer hardware and pharmaceutical industries. I avoid international investments. I spent enough time overseas when I worked in the oil & gas industry to realize that there is little of investment interest outside of the United States. (I'm not alone. Warren Buffett and John Bogle have the same opinion of international investing.) I also avoid real estate. Even though I'm a civil engineer and know my way around a construction site, I've found the equity markets provide higher returns with less hassles and headaches. I've always approached real estate as an expense to be minimized rather than an investment. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

filename = invfor3.html

Copyright © 2001 John P. Greaney, All rights reserved.