![[Retire Early]](retire.gif)

| ............. |

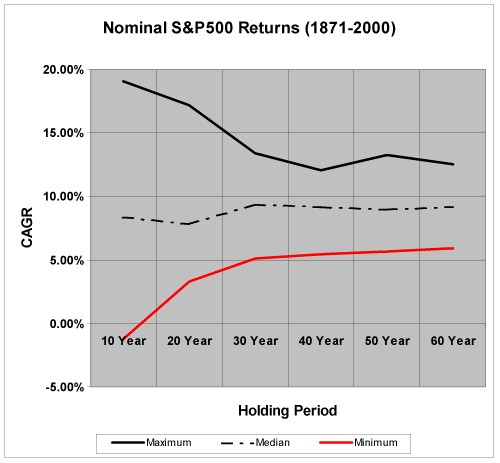

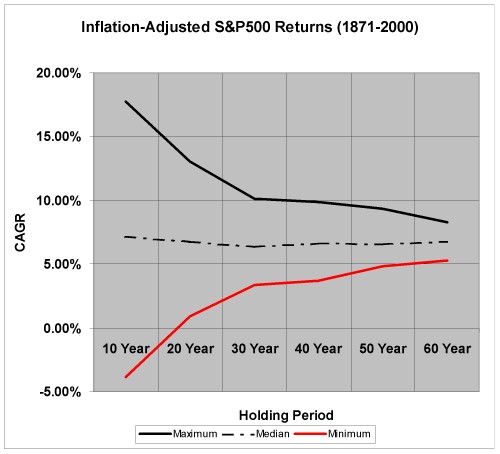

This article was posted on September 1, 2001. Whenever the stock market experiences a decline, many investors seek the safety of fixed income securities. Unfortunately, bonds make poor long-term investments. While it's true that you can get guaranteed returns with US Treasury securities, what's being guaranteed is a "worst case" return when compared to equities. For example, the table below shows the best, worst, and median compounded annual growth rates (CAGR) for the S&P500 for various holding periods from 1871-2000. A 30-year 9.37% compounded annual growth rate means a $1,000 investment grows to $14,687 in 30 years. The current yield on the 30-year US Treasury bond is 5.42% just slightly more than the worst case 5.13% average annual return of the S&P500. -------Nominal S&P500 Returns (1871-20000 Shiller database)---------- ... Holding Period 10-Year 20-Year 30-Year 40-Year 50-Year 60-Year ... Maximum 19.08% 17.14% 13.40% 12.03% 13.23% 12.53% Median 8.33% 7.81% 9.37% 9.14% 8.98% 9.18% Minimum -1.23% 3.30% 5.13% 5.44% 5.65% 5.91%  The news isn't any better for inflation-adjusted returns. The yield on the 30-year Treasury Inflation Protected Security (TIPS) is 3.38% -- just slightly ahead of the worst case 30-year return on the S&P500 of 3.35%. It's even worse if you buy I-bonds today since their yield is only 3.00%. ---Inflation-Adjusted S&P500 Returns (18871-2000 Shiller database)---- ... Holding Period 10-Year 20-Year 30-Year 40-Year 50-Year 60-Year .... Maximum 17.72% 13.06% 10.14% 9.84% 9.31% 8.28% Median 7.12% 6.76% 6.35% 6.58% 6.54% 6.77% Minimum -3.87% 0.89% 3.35% 3.67% 4.83% 5.26%  Once you're retired you should keep a minimum of 5 years' worth of living expenses in fixed income securities, but you shouldn't do that while you're saving for retirement. Stocks or other assets with higher long-yerm average returns are more appropriate while you're accumulating your retirement portfolio. |